In both cases, rates of expansion driven by increase in aggregate business activity resulted in the highest composite output index since June 2010 and the fastest in close to 14 years.

Indian private sector output expanded at a faster pace in April as economic growth across the sector continued to strengthen, buoyed by expansion in buoyant demand from domestic and external clients and a pick-up in sales growth. According to the HSBC Flash India PMI® data on Tuesday, positive demand trends fueled new business intakes and output, taking the headline HSBC Flash India Composite PMI Output Index – a seasonally adjusted index that measures the month-on-month change in the combined output of India’s manufacturing and service sectors – from 61.8 in March to 62.2 in April.

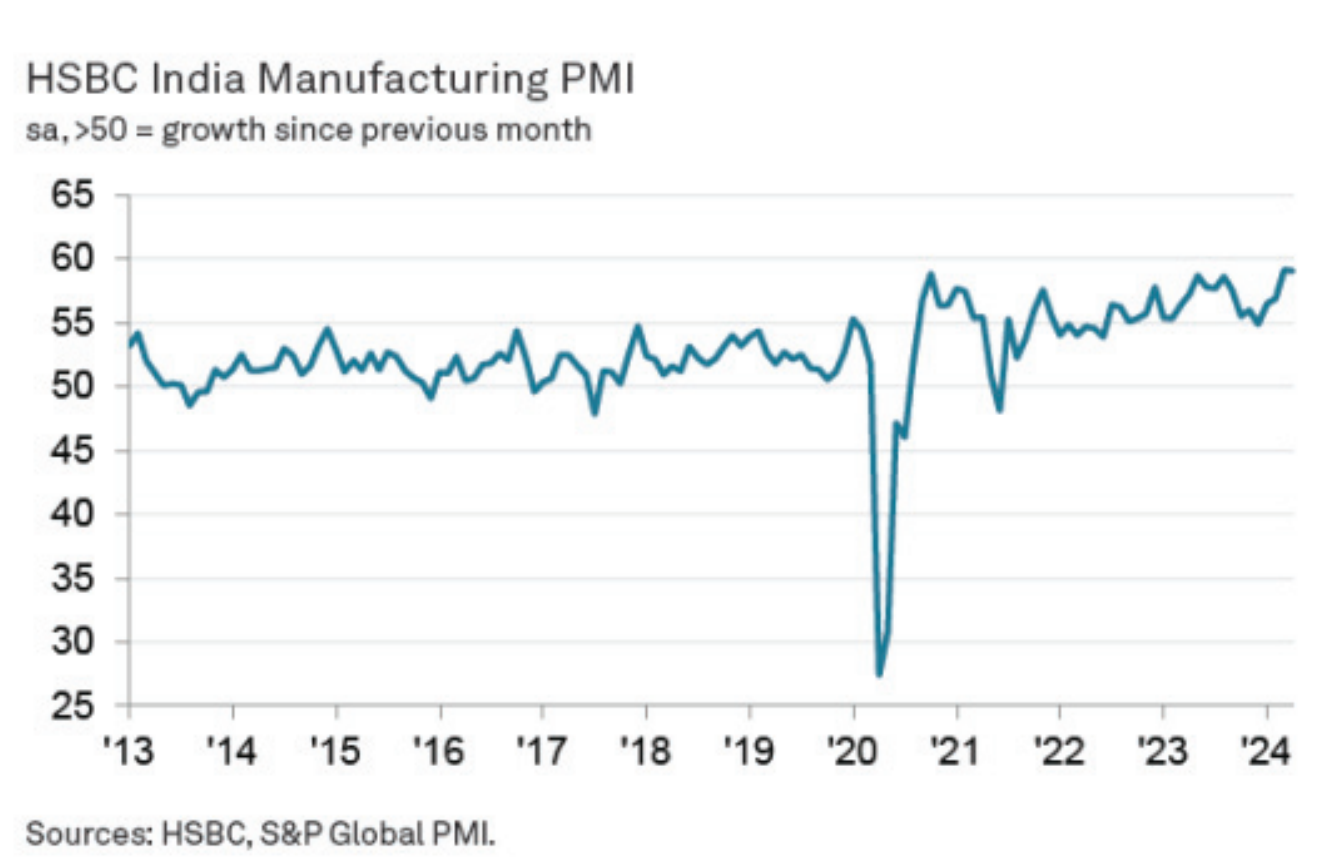

In both cases, rates of expansion driven by an increase in aggregate business activity resulted in the highest composite output index since June 2010 and the fastest in close to 14 years. The manufacturing industry led the latest upturn, as was the case in March, although softening growth at goods producers compared with accelerations at service providers. Sustained increases in new orders added pressure on the capacity of manufacturing firms and their services counterparts, which in turn underpinned recruitment. Jobs growth was notably stronger among the former.

The Reserve Bank of India had noted strong prospects of the manufacturing and services sectors as among factors in pushing the Central Bank for a vote to keep the policy repo rate unchanged at 6.50 per cent. Pranjul Bhandari, Chief India Economist at HSBC, notes that services growth accelerated further in April as new orders in both domestic and international markets rose. “Both composite input and output prices moderated in April, albeit remaining robust. Manufacturing margins improved in April as firms were able to pass on higher prices to customers due to strong demand conditions. In fact, manufacturing industries sharply increased their staffing levels and input buying activity,” says Bhandari, emphasizing improvement in overall future business outlook in April.

Growth in India remained broad-based across the manufacturing and service sectors. The former saw the sharper rate of increase, albeit one that was softer than in March. In the service economy, business activity rose to the greatest extent in three months. Private sector sales expanded for the 33rd successive month in April. In line with the recent trend, international sales positively contributed to total order books. In fact, at the composite level, new export orders rose at the fastest rate since the series started in September 2014. On this front, services companies noted the quicker rate of expansion. Anecdotal evidence pointed to stronger sales to clients in Africa, Asia, Australia, the Americas, Europe, and the Middle East.

Despite persistently robust increases in new business, pressures on capacity remained mild in April. Orders pending completion among private sector companies in India rose for the 28th month in a row, but at a slight pace that was weaker than that recorded in March. Manufacturers also substantially stepped up input buying, with growth climbing to a ten-month high. This supported a further increase in stocks of purchases, one that was the second-fastest since May 2023. Suppliers were reportedly able to accommodate for the upturn in buying levels, with delivery times improving to the greatest extent in ten months.

Yet, efforts to meet rising demand and clear backlogs supported further job creation at the start of the 2024/25 fiscal year. A slight increase in private sector employment masked notable divergences at the sector level. While service providers took on extra staff at a marginal pace that was softer than in March, goods producers raised workforces to the greatest extent in nearly a year-and-a-half.

The survey’s price measures showed slower rates of inflation for both aggregate input costs and output charges. Input cost inflation receded at both manufacturing companies and their services counterparts, with the latter noting the faster rise. Anecdotal evidence suggested that labour costs were the main factor behind rising expenses at service providers. At the composite level, the rate of increase was below its long-run average. Although prices charged for Indian goods and services rose to a lesser extent in April, the rate of inflation remained above its long-run average. According to survey participants, demand strength facilitated the passing on of rising expenses to clients. A stronger increase in the manufacturing industry contrasted with a slowdown at services firms.

Finally, the latest results showed a pick-up in business confidence during April. The composite Future Output Index rose from March’s four-month low and was above the series average (since April 2012). Panelists expect further improvements in demand and productivity over the course of the coming 12 months.